By DMR Law Firm 1. Introduction Establishing a company in Ethiopia requires compliance with a legal and administrative framework designed to regulate business formation, ownership, governance, taxation, and commercial activities. The enactment of the Commercial Code of Ethiopia Proclamation No. 1243/2021 introduced significant reforms by modernizing company structures and recognizing …

The Council of Ministers Investment Incentive Regulation No 517/2022 done on July 12,2022 provides investment incentives for mining, petroleum, geothermal and biofuel works.

In the case of mining, the Regulation states that any holder of exploration license, small scale or large scale mining license or their contractors are allowed to import into Ethiopia equipment, machineries and consumables that are required for their operation or expansion thereof with the work program approved by the Ministry of Mines free from custom duties. In addition to this, the holder of a mining license may import free from custom duties aircraft, helicopter, drones or other exploration equipment for the purpose of collecting relevant information for the mining activities after securing recommendation from the Ministry of Mines.

The holder of a mining license who is unable to import equipment and machinery at pre-development stage may import such goods within 5 years from the commencement of production free of custom duties. Here the holder of artisanal mining license or the holder of any construction mineral mining license issued for the mining of sand or selected materials shall not be entitled to exemptions from custom duties and taxes. The holder of handicraft license or a refinery license who is engaged in the export of minerals may import equipment and machinery that are needed for its operation free from customs duties for 3 years from the date of issuance of such license.

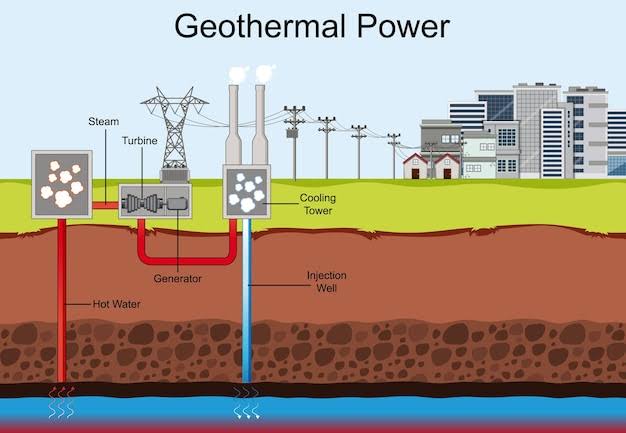

Regarding petroleum and Geothermal works, any holder of petroleum or geothermal license or their contractors are entitled to import into Ethiopia all drilling , geological, Geo physical, production, treating, processing, transportation and other machinery and equipment necessary in petroleum and geothermal operations including aircraft, vessels and other transportation equipment and parts thereof, fuels, chemicals, lubricants, films, seismic tapes, house trailers, disassembled prefabricated structures and other materials necessary for petroleum and geothermal operations free of customs duties of any kind. Expatriate employees of a petroleum license holder or her contractor shall be entitled to import into Ethiopia household goods and personal effects free of customs duties of any kind in accordance with prevailing laws.

Consumables mentioned under mining, petroleum and geothermal operations include chemicals, dynamite and other materials to be used for mining, petroleum and geothermal activities to be specified in a directive to be issued by the Ministry of Finance.

Last but not least, the holder of a biofuel license is entitled to import equipment and machinery free of customs duties for 5 years from the date of issuance of the license based on the work program approved by the regulatory agency.

Concerning transfer of such freely imported items, transfer cannot be made to third parties without having obtained permission from the Ministry of Finance and pay the required duties. However such items may be re-exported free from customs duties or transferred to persons with similar duty privileges upon permission of the regulatory institution.

For any inquiries on your investment in mining and related activities you may contact us at info@dmethiolawyers.com

The investment objective of Ethiopia is to improve the living standards of the people of Ethiopia by realizing a rapid, inclusive and sustainable economic and social development. To achieve such an objective, the Ethiopian government has put in place investment incentives on income tax exemptions and custom duty incentives by Council of Ministers Investment Incentive Regulation No 517/2022 done as of July 12,2022.

Income Tax Exemption Incentives

Any investor who formed a new company or any existing investor expanding or upgrading her investment shall be entitled to income tax exemptions, as provided in the schedule attached to the Regulation. Those investors who have invested outside of the industrial park and who engage in export or supplies to an exporter as production or service input, at least 60% of their products and services shall be entitled to additional years of income tax exemption in addition to those provided in the schedule. The commencement period of income tax exemption is as of the date the investor obtained a business license or from the date the investor obtained expansion permit. However, the investor who has incurred loss within the period of income tax exemption period shall be allowed to carry forward such loss for half of the income tax exemption period after expiry of such period.

Custom Duty Incentives

New investor or an investor expanding or upgrading existing investment engaged in one of the investment areas specified in the Schedule, may import duty free capital goods and construction materials necessary for the establishment of a new investment or the expansion or upgrading of an existing investment. Total or partial exemption of motor vehicles from customs duty shall be determined by Directive to be issued by the Ministry of Finance. Such imported capital goods or construction materials imported free of customs duty may be transferred to persons with similar duty free privileges. Otherwise custom duty has to be paid to transfer to those persons who have no similar duty free privileges. The investor may re-export the duty free imported capital goods or construction materials.

Regulatory Institutions

The Ethiopian Investment Commission, Ministry of Finance, Ministry of Mines, Regional Governments, Addis Ababa and Dire Dawa City Administrations Investment Organs, Ministry of Trade and Regional Integration, Ministry of Revenue and Customs Commission are assigned common and specific duties and responsibilities to implement and follow up the implementation of investment incentives.

Revocation of Tax Incentives

Any investor whose investment license is revoked shall return all investment incentives acquired. The Ministry of Finance shall determine the manner of return of investment incentives improperly acquired.

Conclusion

To encourage investment in Ethiopia, the Ethiopian government has provided for its investors income tax exemptions and custom duty exemption privileges. The regulatory institutions duties and follow ups are defined so as to enable smooth implementation of the investment incentives to new investors or those investors expanding or upgrading their investment.

For further information, please contact Mahlet at info@dmethiolawyers.com

This article summarizes the Federal Supreme Court Cassation Decision on File No 215383 on 30/05/2022. The adoption case is filed by the 1st and 2nd applicants, namely Wro Arsema and Mr.Yergen. There is no respondent on the case. The case is about whether or not a foreigner husband can adopt his step daughter who is the child of his Ethiopian wife?

Federal First Instance Court

The Applicants filed in the Federal First Instance Court for an approval of their adoption agreement. The child involved in the adoption is the child of the 1st applicant born prior to her marriage with the 2nd applicant. The second applicant who is the adopter of such stepchild is a Dutch nationality. The court said that due to Revised Family Code (Amendment) Proclamation No 1070/2018, adoption of an Ethiopian child by a foreigner is prohibited. Thus the applicants request of approval of their adoption is dismissed by the court.

Federal High Court Appeal

The Applicants submitted an appeal to the Federal High Court. However, the Federal High Court upheld the decsion of the Federal First Instance Court.

Review by the Federal Supreme Court Cassation Bench

The Applicants presented their application for basic error of law to the Cassation Bench. The Applicants stated that the applicants are married in Ethiopia, have a son together and living in Ethiopia. The child to whom the adoption is requested is the daughter of the 1st applicant and not that of the 2nd applicant. Nowadays, this daughter lives together with her step father, who is the 2nd applicant and even uses his name as father’s name as well. The Applicants argued, to enable such a daughter with equal status to her brother, who is born from both the applicants, the adoption by the step father is necessary. The Applicants said, rejecting our request for approval of such an adoption by the lower courts is not in the best interest of our daughter. Thus the Applicants demanded for the dismissal of the lower court’s decision.

The Cassation bench accepted the request of the Applicants for review. The Cassation Bench identified the issue of whether Proclamation 1070/2018 is meant to prohibit adoption occurring between spouses or not?

The Cassation Bench raised the issue of the appropriate law to govern the case: is it Revised Family Code Proclamation 213/2000 or Proclamation No 1070/2018? The provisions of Proclamation No 213/2000 Article 187 provide the fact that married couples can adopt a child together or when the child to be adopted is one of the spouses only, the adoption by the other spouse is possible. This provision of the Revised Family Code does not stipulate nationality of the spouses as a precondition for an adoption. This provision doesn’t state the adoption of a child of one spouse by the other spouse is allowed only for Ethiopian married couples.

On the other hand, Proclamation No 1070/2018 contains provisions that order the cancellation of provisions of the Family Code Proclamation No 213/2000 Articles 193, 194(3)(d) and (4) that contain the word ‘the adopter being a foreigner’. The Cassation court argued that the provision of Article 187 of the Revised Family Code is not deleted or amended by Proclamation No 1070/2018. Thus, the request of adoption of a child of the Ethiopian spouse born prior to the marriage to a foreigner spouse cannot be rejected mentioning Proclamation No 1070/2018. Specially given the fact that the spouses are married in Ethiopia and residing in Ethiopia as a couple. Therefore, the Cassation Bench concluded that the lower court’s decision rejecting the adoption approval request of the Applicants is dismissed for basic error of law. The Cassation Court ordered the Federal First Instance Court to look into the matter from this perspective and pass a decision on the adoption approval request of the Applicants.

Conclusion

A foreign national spouse who is married to an Ethiopian national can adopt an Ethiopian child of his Ethiopian spouses and the Revised Family Code(Amendment) Proclamation No 1070/2018 is not intended to stop such an adoption request.

For further request on the subject, you may contact us at info@dmethiolawyers.com

The Federal Government of Ethiopia and the Tigray Peoples’ Liberation Front (TPLF) has signed a peace agreement to end the two year war in the northern part of Ethiopia in an African Union mediated talks in Pretoria South Africa on 2nd of November, 2022. The agreement signed signals the permanent cessation of hostilities for a lasting peace and the agreement incorporates 15 provisions in addition to its preamble. The effective date of the agreement is the 3rd of November,2022.

One of the investment incentives in Ethiopia for foreign investors is the privilege of opening bank accounts and operating the same. The Investment Proclamation No 1180/2020 allows foreign investors to open and operate foreign currency accounts in any private bank in Ethiopia for the purpose of their investments. Foreign Investors are defined as an individual or company who has invested foreign capital in Ethiopia. The manner of operation of foreign currency account is determined by the directives of the National Bank of Ethiopia. The National Bank of Ethiopia has issued a directive that is effective as of November 9,2020 namely “Establishment and Operation of Foreign Currency Saving Account for Residents of Ethiopia, Non-Resident Ethiopian and Non-Resident Ethiopian Origin” Directives No. EX1V 68 /2020″ that allows foreign investors who are residents of Ethiopia to open and operate foreign currency accounts in addition to that of local savings or current accounts of their choice.

For your investment inquires you may contact us at info@dmethiolawyers.com